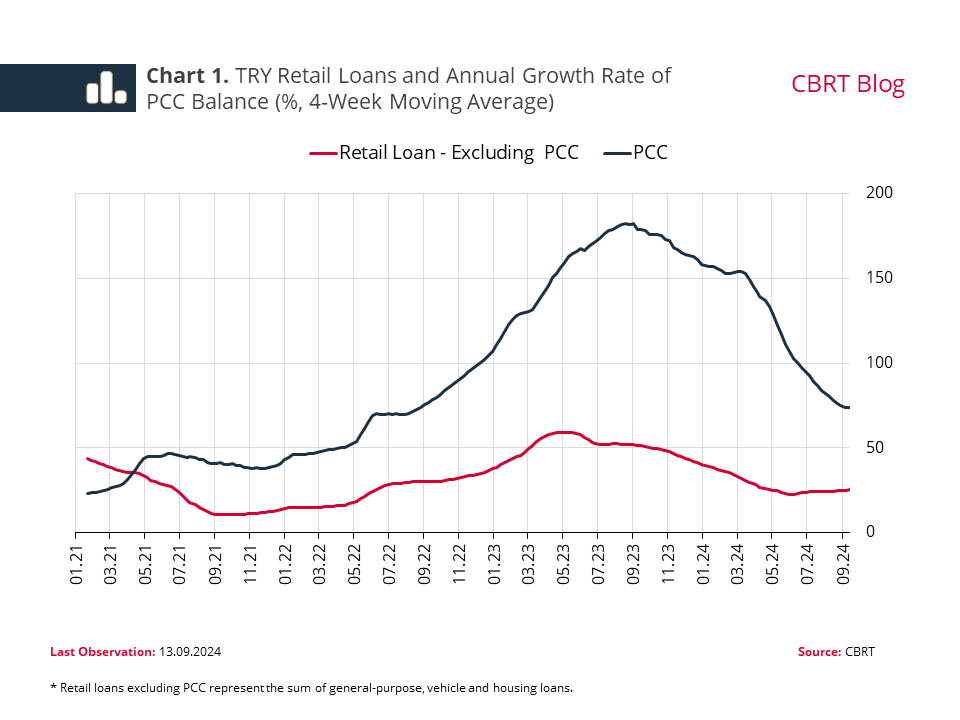

The personal credit card (PCC) balance is growing faster than other retail loan types (Chart 1). The annual rate of growth in PCC balance increased up to 180% in 2023. This growth is driven not only by demand-led developments but also by the use of credit cards as a means of payment. This blog post explores the breakdown of PCC balances at a granular level.[1] Results reveal that the majority of card users have low debt balance, and the total balance is concentrated on a small number of card users with large debt balances.

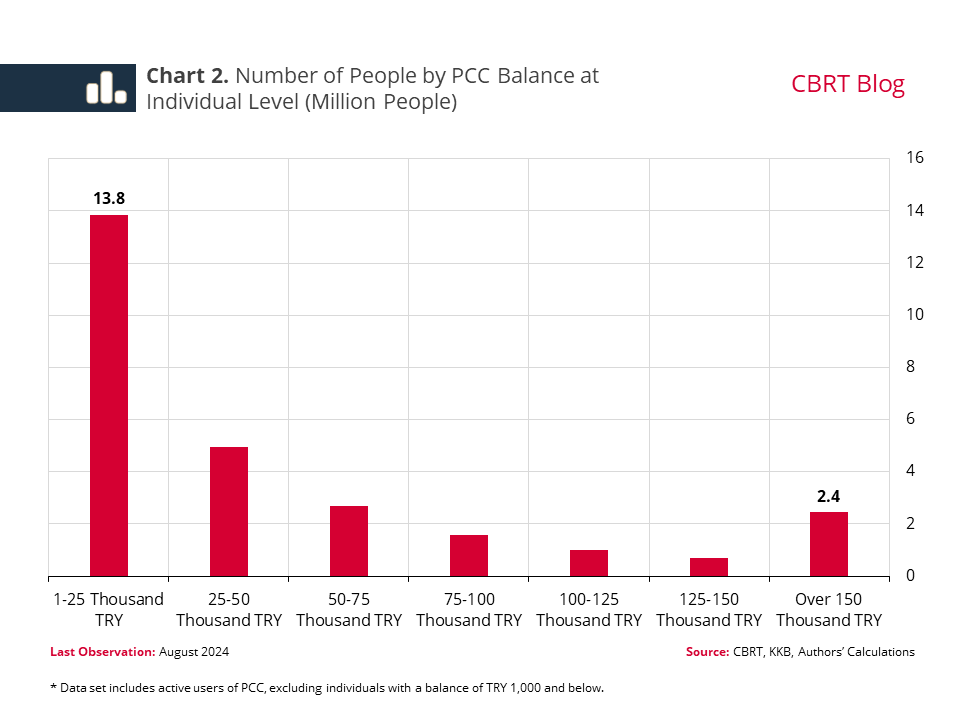

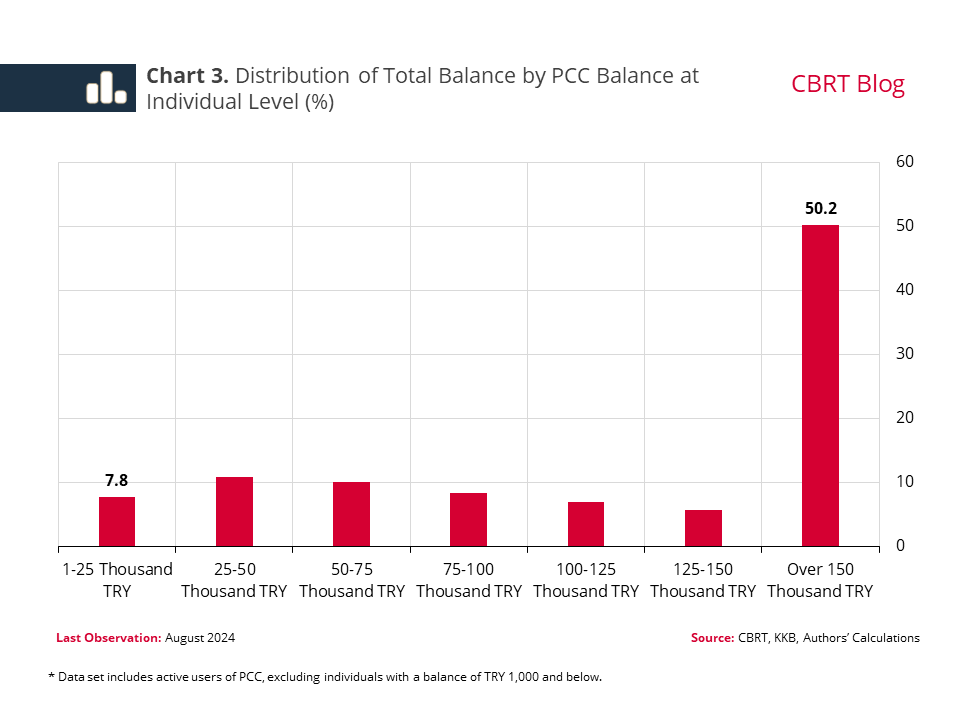

Of 28 million active PCC users, approximately half (14 million people) have a balance below TRY 25,000.[2] We see that the number of users is significantly smaller in larger debt balance categories and the number of card users with a debt above TRY 150,000 accounts for 9% of all users (Chart 2). Simultaneously, the share of this group in the aggregate PCC balance exceeds 50% (Chart 3).

Taking into account the widespread use of PCC by households and their role in facilitating the consumption-smoothing on a monthly basis, the maximum contractual interest rate is set below the rates for other retail loan types.[3] This encourages borrowing and consumption through the use of PCC as a credit instrument. Using the PCC as a credit tool by delaying due payments appears to be more common among persons with high debt balances. On the other hand, delaying due payments is less common for users with low debt balances who make up the majority of card users. Therefore, there seems to be ample motivation for an adjustment in regulations that will reduce the delaying motivation of the users with high debt balance. The CBRT’s recent regulation to differentiate maximum contractual interest rates for credit cards based on card balances should be evaluated in this context.

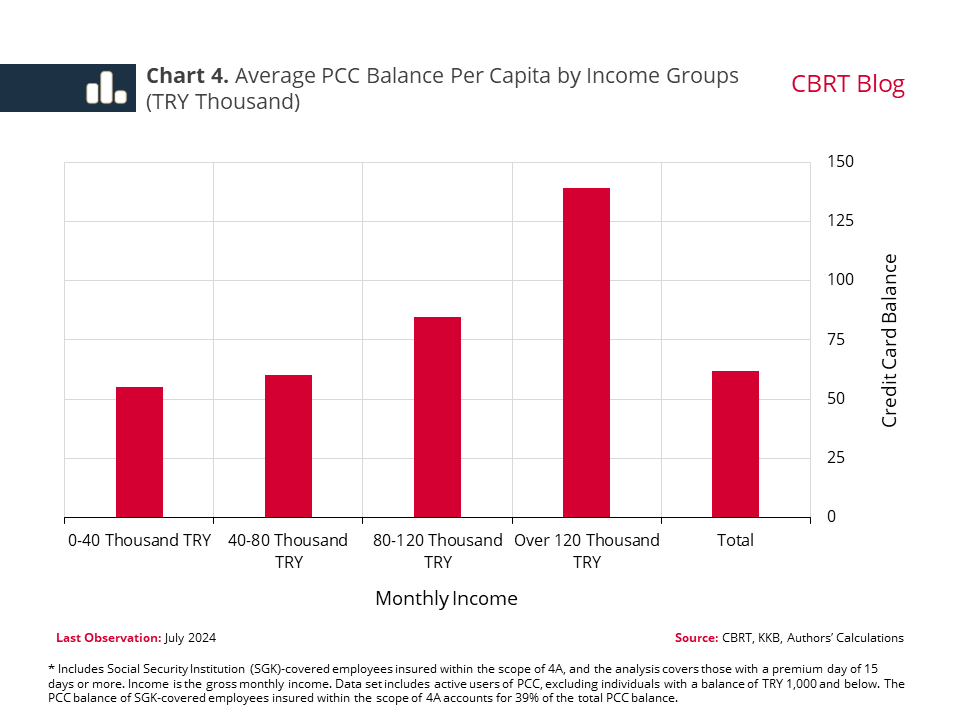

The heterogeneity among the PCC balances across card users is also largely consistent with their income levels (Chart 4). According to our calculations based on the administrative records of wage earners, the PCC balances are higher among higher income groups. It is notable that high PPC balances are concentrated on the upper quantile of the gross monthly income distribution. The CBRT’s latest regulation is therefore expected to have a tightening impact on the PCC balance growth of high-income individuals.

To sum up, by differentiating the maximum contractual interest rates for credit cards based on balances, the CBRT incentivizes a reduction in credit card indebtedness and contributes to the rebalancing in domestic demand. The Banking Regulation and Supervision Agency’s simultaneous introduction of a debt restructuring program for credit cards with overdue minimum payments ensures that individuals with currently overdue debts will be minimally affected by this tightening policy. The macroprudential measures taken in a close coordination between the institutions are thus supporting the disinflation process.

[1] Individuals are estimated to hold two credit card accounts on average. In all analyses using micro data, individuals’ credit card accounts have been aggregated at individual level. In the CBRT’s regulation differentiating interest rates based on credit card term debt, credit card accounts are taken into account.

[2] Analyses are based on 27 million card users with a total credit card balance above TRY 1,000.

[3] The average annual compound interest rate for general-purpose loans is 72.3% as of September 2024, while the annual compound maximum contractual interest rate for credit cards is 65.9%.